")

THE POLITICAL AND FINANCIAL COST OF INTERNATIONAL CONFLICTS

The Archivio Disarmo International Research Institute recently published in its journal 'IRIAD Review. Studi sulla Pace e sui conflitti’ (IRIAD Review: Peace and Conflict Studies'), an in-depth look at the cost of international conflicts. We are pleased to republish it here, and thank the experts of Archivio Disarmo for their collaboration.

2024 proved to be a year of growing tensions: from the conflict in Ukraine, which continues to rewrite the strategic priorities of Europe and beyond, to the escalating conflicts in the Middle East and the competition between the US and China. In the course of the year, the consequences of strategic and military choices made in the 2022-2023 biennium emerged strongly. The geopolitical priorities were reflected in the record increase in global military spending and in the re-emergence of the nuclear threat, which in turn fuelled international dynamics.

In a world that appears increasingly divided, nuclear doctrines are undergoing significant transformations. The recent revisions of nuclear policy by Russia and the United States reflect an increasingly polarised world, where the role of atomic weapons returns to the centre of security strategies and the risk of global escalation increases.

Although the overall number of nuclear warheads has decreased, the volume of ready-to-use warheads has increased, reaching 9,585 warheads out of a total of 12,121 in January 2024. The number of deployed forces has risen to 3,904 (60 more than the previous year), with 53.79% in a state of maximum operational alert for ballistic missiles. Russia and the United States hold almost 90% of the world's nuclear weapons, although they each have over 1,200 warheads currently being decommissioned.

The nuclear arms race is not limited to the traditional powers. India, Pakistan and North Korea are also increasing their potential. Pakistan continues to invest in deterrence against India, while the latter is expanding its long-range weapons capabilities, especially towards China. North Korea, which has about 50 warheads already assembled and fissile material for another 40, is focusing on the use of tactical nuclear weapons, with new short-range ballistic missiles and cruise missiles for land attacks. Finally, Israel, which, moreover, does not officially acknowledge that it possesses nuclear weapons, is allegedly modernising its capabilities and increasing its plutonium production, hampering efforts to create a Middle East zone free of nuclear weapons and weapons of mass destruction. In the region, attacks by Iranian-backed groups against US forces in Iraq and Syria are further complicating the tensions between Tehran and Washington, disrupting recent attempts at détente.

Military expenditure in the years 2014, 2022 and 2023, with GDP share for 2023.

| Ranking | Country | Year | Share of GDP (2023) | ||

|---|---|---|---|---|---|

| 2014 | 2022 | 2023 | |||

| 1 | United States | 647,789.0 | 860,692.2 | 916,014.7 | 3.4 |

| 2 | China | 182,109.2 | 291,958.4 | 296,438.6 | 1.7 |

| 3 | Russia | 84,696.5 | 102,366.6 | 109,454.4 | 5.9 |

| 4 | India | 5,914.1 | 79,976.8 | 83,574.6 | 2.4 |

| 5 | Saudi Arabia | 8,762.4 | 70,920.0 | 75,813.3 | 7.1 |

| 6 | United Kingdom | 6,995.5 | 64,081.6 | 74,942.8 | 2.3 |

| 7 | Germany | 4,662.8 | 56,153.1 | 66,826.6 | 1.5 |

| 8 | Ukraine | 3,961.6 | 41,183.9 | 64,753.2 | 36.7 |

| 9 | France | 53,134.8 | 53,638.7 | 61,301.3 | 2.1 |

| 10 | Japan | 46,903.5 | 46,880.2 | 50,161.1 | 1.2 |

Source: SIPRI (2024a) in mln US dollars at current prices

It should be emphasised that the modernisation of nuclear arsenals is not taking place in isolation: it is part of a broader context of increasing global military expenditure. The data show that the defence budgets of many powers are increasingly geared towards funding both nuclear capability and the expansion of conventional armaments.

Not surprisingly, the increase in global defence investment is not limited to the nuclear sector. The crises that mark the current international scene are directly reflected in an unprecedented increase in global military expenditure. Let us then analyse the main trends that have emerged from Sipri (Stockholm International Peace Research Institute) data, highlighting how global powers are also devoting increasing resources to conventional armaments. Such investments reflect the perception, whether justified or not, of increasing threats and contribute to fuelling a spiral of global insecurity.

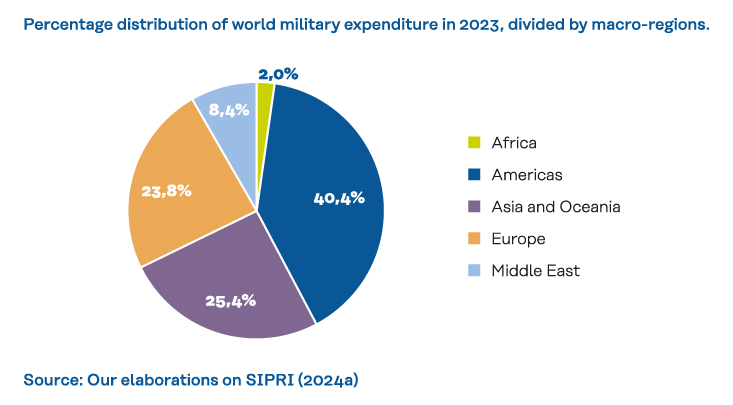

According to the Sipri 2024 report, 2023 was a record year for global military spending, which reached USD 2,443 billion or 2.3% of the world's Gross Domestic Product. This leap was the fastest growth since 2009. For the first time in over a decade, military spending increased simultaneously in all five geographical regions of the world. The 5 countries with the highest expenditure are the United States, China, Russia, India and Saudi Arabia, which together accounted for 61% of world military expenditure.

In Europe, military spending reached USD 588 billion in 2023, an increase of 16% compared to 2022 and of 62% compared to 2014, following the war between Russia and Ukraine. In Central and Western Europe, total military expenditure reached USD 407 billion, an increase of 10% compared to 2022 and of 43% compared to 2014. The UK remained the largest military financier in the region, increasing military spending by 7.9 % compared to 2022 and by 14 % compared to 2014, accounting for 2.3 % of GDP in 2023. Germany saw a growth of 9% in military spending in 2023 and 48% compared to 2014. Currently, the military burden makes up 1.5% of the GDP, but the German government has pledged to reach 2% cent of the GDP as of 2024. The largest annual increase among European countries is in Poland, with 75% growth since 2022 and 181% compared to 2014. This is 3.8% of the GDP, with the government hoping to bring this figure to 4%. In April 2023, Finland joined NATO.

The incidence of military expenditure (expressed as a percentage of the GDP) provides a key to assessing the weight that national economies attach to defence compared to other priorities. Sipri estimates that this burden increased globally from 2.2% of the GDP in 2022 to 2.3% in 2023. The Middle East recorded the highest military burden (4.2% of the GDP), followed by Europe (2.8%), Africa (1.9%), Asia and Oceania (1.7%) and the Americas (1.2%). The military burden grew significantly in Europe (+0.5%), the Middle East (+0.5%) and Africa (+0.2%), while it remained unchanged in the Americas, Asia and Oceania. The global increase highlights a worrying trend towards an ever greater economic commitment to the military, reflecting a spiral of insecurity in which countries, perceiving others' military spending as threatening, respond by increasing their own.